Innovations to spark the future of education

Deloitte & EduGrowth

2017

The inaugural Australian EdTech Market Census paints a picture of a diverse and thriving sector with strong potential to grow. Based on respondents’ stated monthly revenues and number of learners the survey shows that the sector already has revenues of upwards of $1 billion per annum and significant traction with more than 3 million learners using their platforms and solutions. This is particularly heartening in light of the fact that EdTech is a critical enabler for our third biggest export; international education. Technology as a differentiator can give us the edge over global competitors to realise our international education growth aspirations and scale to meet the ensuing demand.

The Australian EdTech market is making a significant contribution to job creation

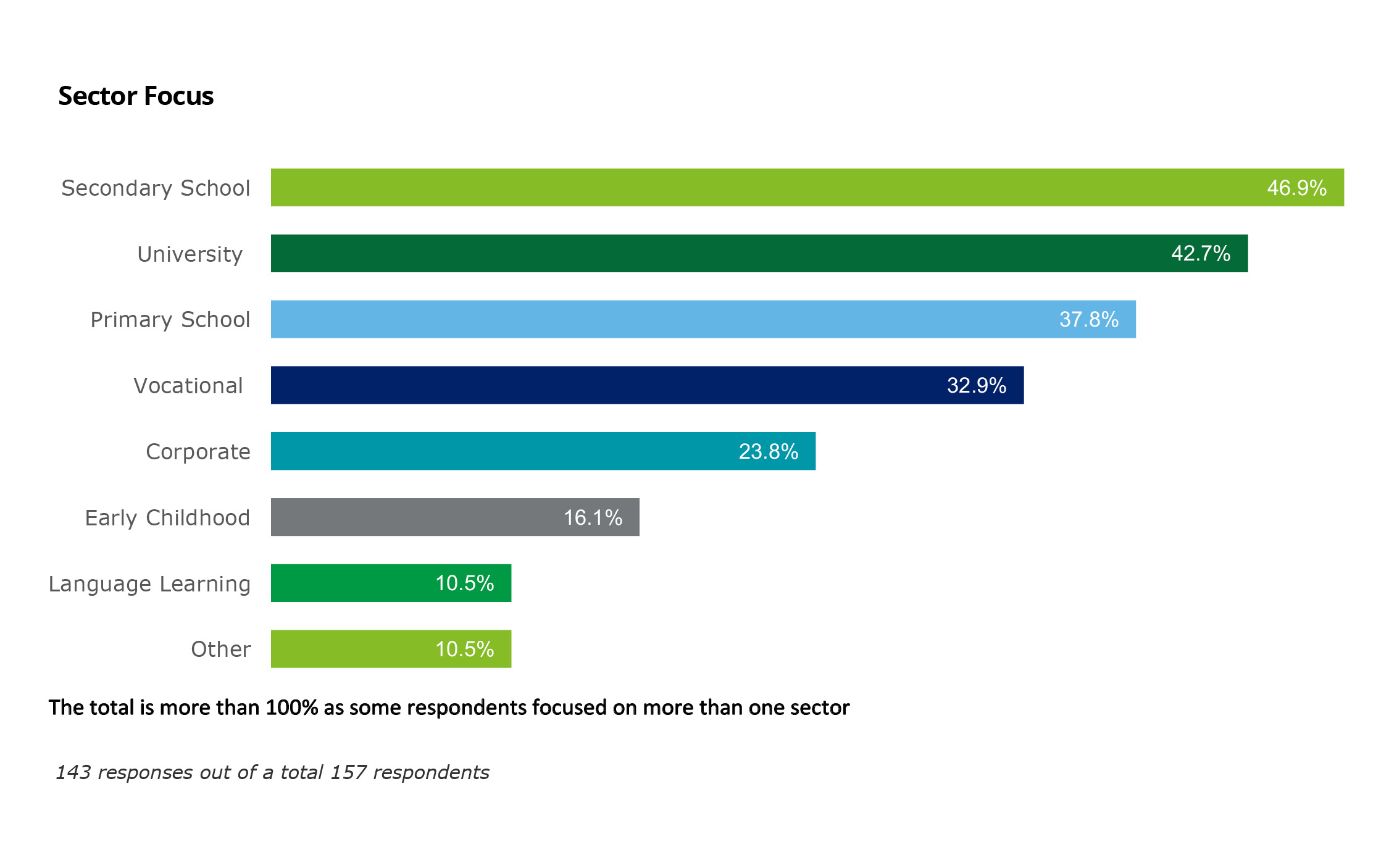

Matching overall revenue spend and focus the EdTech survey shows that the highest percentage of EdTech organisations are focused on secondary schools and universities

With the global EdTech market forecast to grow to $252 billion by 2020 it is also encouraging to see that 46% of respondents’ already have customers outside Australia and 22% of respondents’ have plans to expand overseas. In a global economy characterised by rapid economic restructuring and change, the Australian EdTech market has an important and significant role to play in job creation. The EduGrowth survey shows strong forecast jobs growth in the EdTech sector with 60% of organisations looking to hire in the next six months and 10% of those looking to hire six or more employees in the next six months.

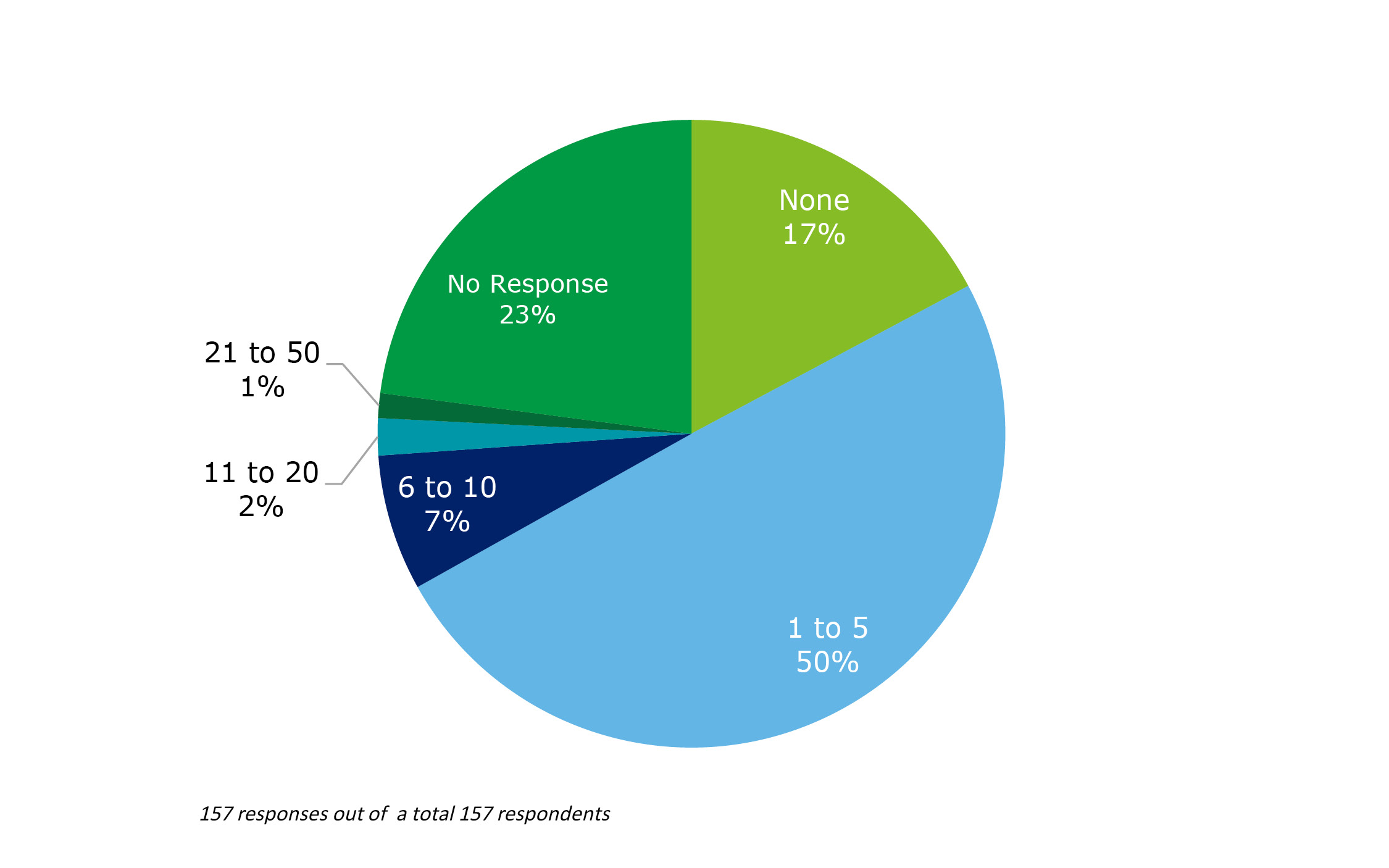

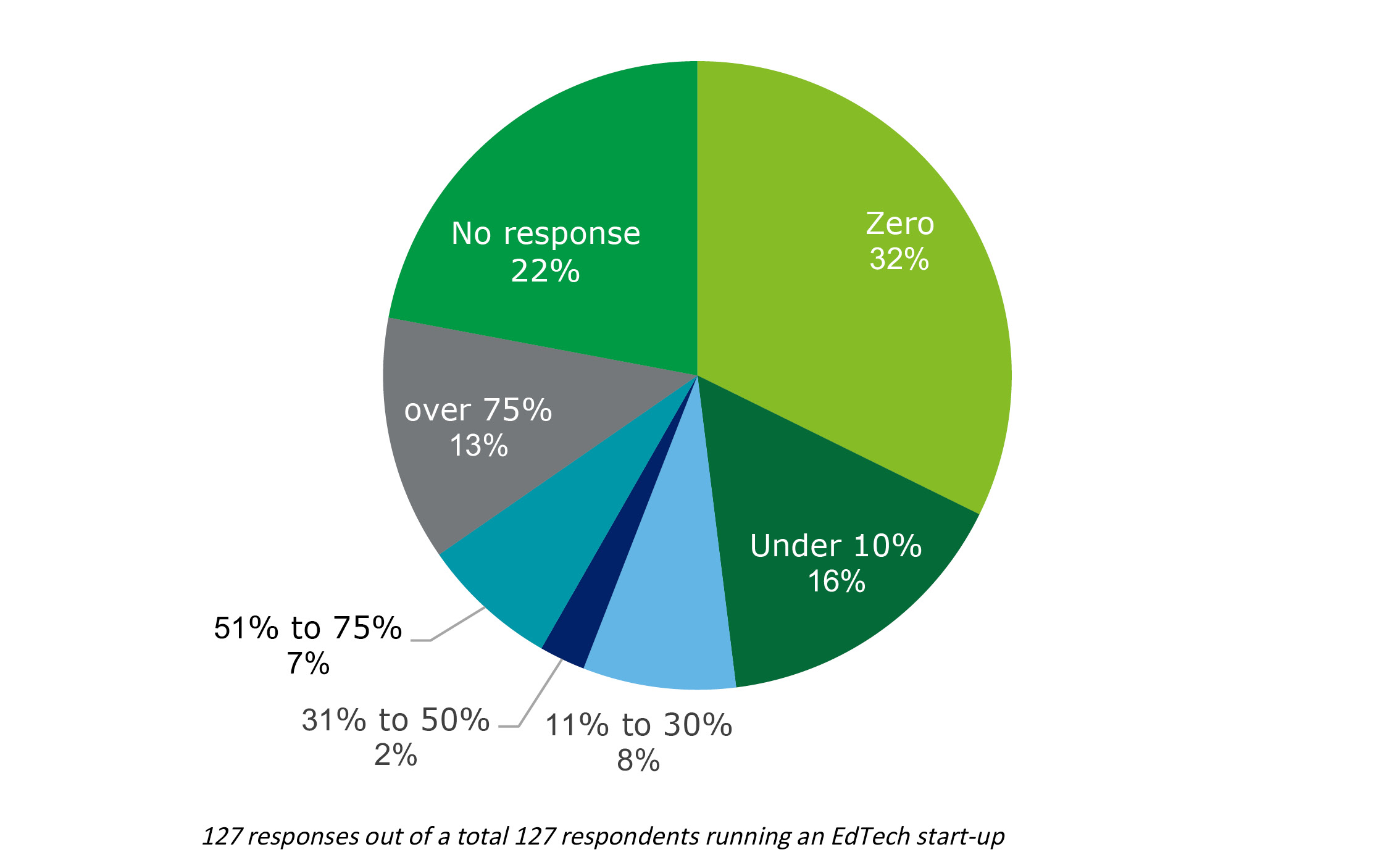

Most of our EdTech start-ups are located in the populous ‘East Coast’ primarily, because, in the fast moving tech sector, proximity and density are critical to a thriving start-up industry. Start-up ecosystems typically need access to talent, funding, clients, technology research, incubators and other start-up mentors. However, the survey also shows that 63% of Australian EdTech start-ups have no capital investment and 29% see raising investment as one of their major challenges in 2017.

The emerging rivals for Australia’s EdTech ‘Silicon Valley’ are all in the East Coast

Australian EdTech organisations are thinking global; 46% have customers outside Australia

At the end of this survey then, if there is one call to action it is that universities, policy makers and businesses all have a significant role to play in ensuring that our nascent and necessary EdTech sector continues to prosper and grow. Policy makers to define settings that attract capital investment into high-potential start-ups, and facilitate the acceleration and commercialisation of early-stage innovations. Universities to develop the research and build the pipeline of workers necessary to fuel the start-ups and wherever possible to help nurture and incubate start-ups. And, likewise, businesses to help nurture and develop talent, invest in high-potential ventures and help incubate and commercialise innovative ventures.

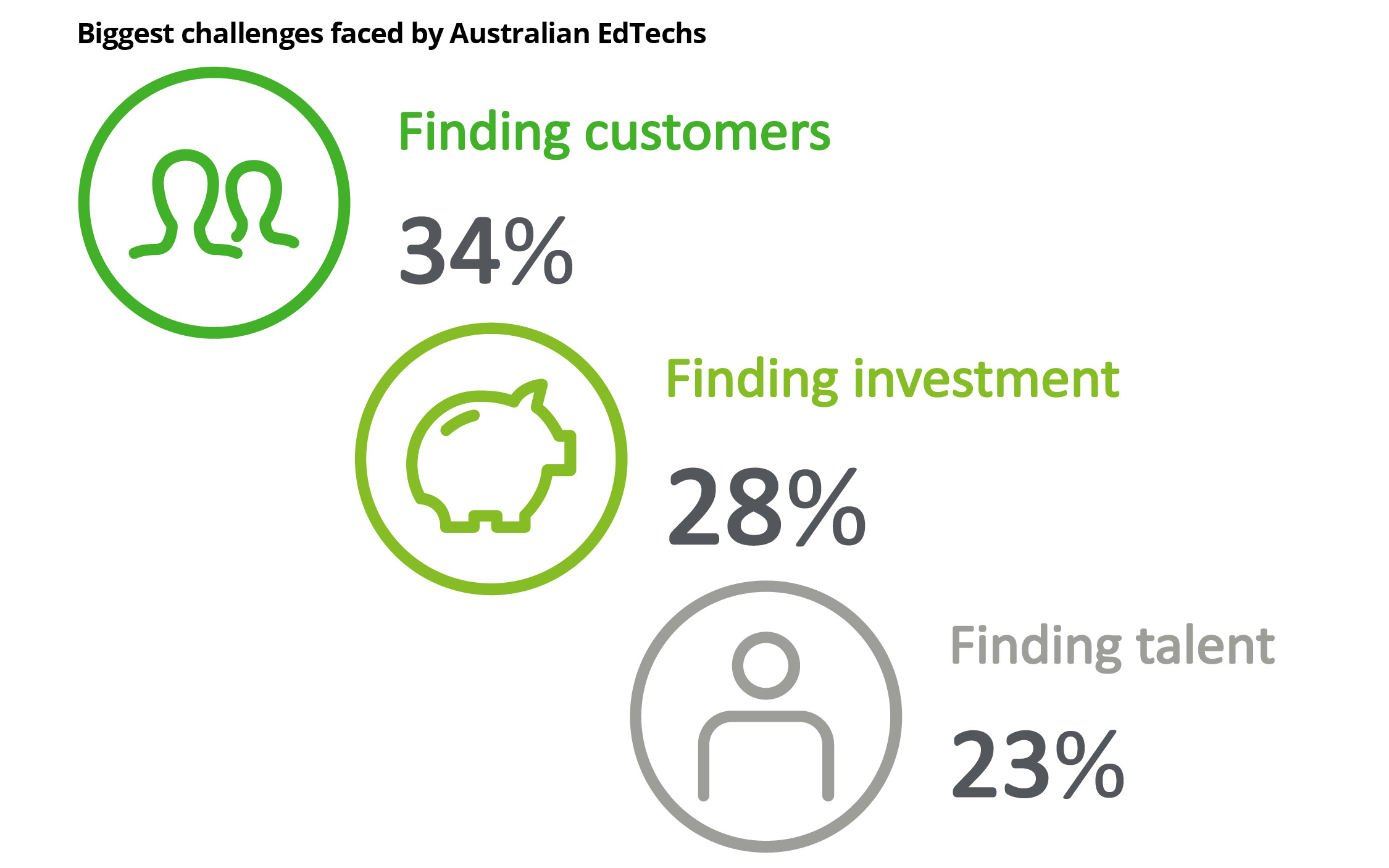

Biggest challenges faced by Australian EdTechs. A tricky trio: finding customers, investment and talent

Register to download report

Note: this page will refresh on submit to reveal the download link